How an Active Fixed Income Strategy May Help Mitigate Reinvestment Risk

From March 2022 through August 2023, the Federal Reserve (the “Fed”) executed one of its most aggressive monetary policy moves in decades, raising the Federal Funds Target Rate (the rate that banks charge each other to borrow or lend excess reserves overnight)over 500 basis points (“bps”) to an ending target range of 5.25%-5.5%. The end result of the aggressive monetary policy was an interest rate environment that many investors had not experienced in years, if at all, in their lifetimes, and had been widely viewed as the end of a 40-plus-year bond bull market. Even after several reductions to the Fed Funds Target Rate in the third and fourth quarter of 2024, the Bloomberg US Aggregate Index® still provides a yield of just under 5.00%, while the Bloomberg US Corporate High Yield Index® offers a yield of about 8.50% (as of date of publication). Hence, we believe this has left investors with an opportunity to potentially earn attractive returns as yields remain near the highest level in more than a decade.

Risk Versus Reward

With a reasonable estimated long-term return assumption of 6% – 7% for U.S. equities from a long-term historical perspective, many investors are considering the plethora of opportunities in the fixed income markets that could potentially rival that performance, while at the same time, seeking to mitigate the risk of loss to their investment principal.

For instance, many investors have recently increased their asset allocation to fixed income through what is generally viewed as the safest and most liquid market, U.S. Treasury Bills. Who could blame them? The yields on 6-month Treasury Bills are currently at about 4.2% in annualized yield to maturity (as of date of publication), while offering investors what has historically been known as the “risk-free rate of return.” By comparison, intermediate maturity investment-grade corporate bonds are currently yielding approximately 5.00%, and high-yield corporate bonds offer yields in the range of 8.25% – 8.50%. So, on the risk/reward spectrum, investors have an interesting set of options. They also need to consider the different characteristics of various fixed income asset classes, and which are best suited for their individual investment needs and tolerance for risk.

As we think about the inherent risks of fixed income investing, primarily credit and interest rate risk, let’s take a closer look. Risk of default (credit risk) for U.S. Treasury Bills is generally considered to be non-existent (especially over a short holding period), while loss of principal from rising rates, as measured by duration (interest rate risk), is similarly remote due to the short maturities. However, this brings us to a risk that has not been widely considered by fixed income investors for many years and perhaps even forgotten: reinvestment risk.

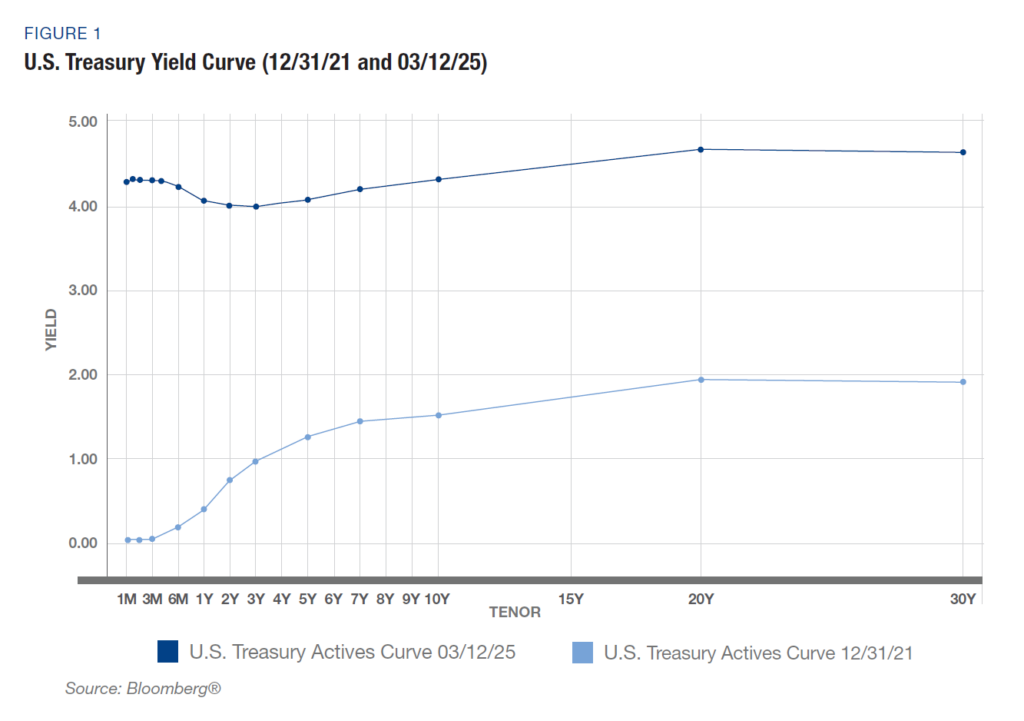

In a “normal” interest rate environment, the yield curve would be positively sloped (see Figure 1 – Yield Curve Dated 12/31/21) to compensate investors for the risk of inflation eating away at their rate of return, as well as the longer-term risk of default. However, in the current interest rate environment, short-term rates and long-term rates are substantially the same (see Figure 1 – Yield Curve Dated 3/12/25), creating what is known as a “flat” yield curve. This flatness, likely the result of the Fed’s previously aggressive monetary policy, as well as investors’ increased appetite for longer-dated Treasury Notes and Bonds to protect against a potential recessionary environment, has created an interesting conundrum. Compelling yields in the front end of the curve appear to be a very attractive option for investors, as they expect to earn about the same or more income by investing in short-term investments compared to longer-dated issues.

However, the reinvestment risk mentioned earlier now comes to the forefront. This lurking risk, unbeknownst to many investors, relates to the “risk” of rates being lower when these short-term investments mature. Although earning approximately 4.3% on an annualized basis for this “risk-free” option, investors might need to consider the future interest rate environment when bonds come due, since that yield may not be available to reinvest maturity proceeds if rates begin to decline. Hence, the possibility, or risk, of earning less income in the future due to a declining rate environment.

So, how do investors navigate the fixed income markets to take advantage of the current rate environment, while potentially mitigating the various associated risks, including reinvestment risk? Credit risk is generally mitigated by in-depth fundamental analysis of an issuer’s credit metrics, while interest rate risk can be monitored by keeping portfolio duration within an investor’s risk profile based upon their individual investment goals and objectives.

As the fixed income markets move toward the possibility of rates remaining range-bound or seeing a more sustainable decline, reinvestment may become a more important risk factor to consider. Yet this risk creates some challenges, especially with the compelling opportunities to earn more income in short maturity investments compared to more interest-rate sensitive, longer duration assets. However, once the risk materializes in a rapidly declining rate environment, it may be too late to react. Therefore, fixed income investors should prepare sooner rather than later by creating a well-diversified portfolio that balances various maturities across the yield curve.

Strategic Considerations:

- Short-term investments offer attractive returns if held to maturity, but longer-term investments may lock in historically high yields.

- If rates decline, the risk of reinvestment at lower yields could be offset by rising bond prices of longer duration assets, as bond prices generally increase when rates fall.

The Role of Active Portfolio Management

The description of the various risk factors referenced above, which include credit risk, interest rate risk and reinvestment risk (to name a few), and the inherently volatile fixed income markets, may make for an overwhelming task for individuals who may hope to enjoy the long-term benefits of a well-diversified bond portfolio. Therefore, investors may wish to consider an active portfolio management approach and the role it plays in helping to mitigate the various risk factors, while seeking high current income and the potential for attractive risk-adjusted returns.

Conclusion

The current interest rate environment, shaped by the Federal Reserve’s aggressive monetary policy and fears of a slowing economy, offers investors compelling opportunities in the fixed income market. However, it also introduces the risk of reinvestment at lower rates as short-term investments mature during a declining rate environment. While yields on short-duration assets including money market securities are attractive, the potential for rates falling in the future calls for careful consideration. To navigate these challenges, investors should consider an active fixed income strategy, emphasizing diversification across maturities and the proactive management of credit, interest rate, and reinvestment risks. By doing so, investors can better position themselves to take advantage of the current yield landscape while mitigating potential risks in the years ahead.

Material prepared by:

David Schiffman | Portfolio Manager and Director of Fixed Income Investments | Cantor Fitzgerald Asset Management